The US Election results, combined with continued concerns in Europe, brought a volatile end to the 2016 muni campaign. Now, as we approach 2017, there seems to be nothing but concern for higher interest rates and damaged muni value, due to lower tax rates in the future. We feel the market ended 2016 discounting some of this potential bad news and, going forward, the market does not seem to know what to expect. We see 2017 as the year of the Gray Swans in the municipal market.

The Gray Swan, yes a hybrid of the Black Swan, is an event that can be anticipated to a certain degree, but the degree of its impact on the valuation of a security or the health of the overall market is not certain. There is history that shows what has happened in the past, but the potential impact this time on the market is difficult to quantify, as conditions are not always the same.

What Gray Swan events are we concerned with in 2017?

- Income and Corporate Tax Reforms – We know they will both be attempted by the new administration. Whether they are enacted and to what degree, are still open for debate.

- A Large Infrastructure Funding Program – Are we finally going to get this thing going? If so, how big and how will it be funded?

- Fiscal Stimulus and its Impact on Interest Rates – Are you a person who believes we are at the end of the low interest rate cycle? Is inflation really about to return? What is the impact on US rates given negative interest rates in over 70% of the world markets?

- Credit concerns on the Muni Horizon – There are some problem children out there who just can’t seem to behave themselves. Will this be the year one of them gets kicked out of the sandbox?

All of the above events have occurred in the past at some point. However, this time around, they are all in the same pond at the same time. Add in (what we feel) will be a more volatile muni market going forward, and you can see why we are entering 2017 with concerns that are hard to handicap. We will do our best in this outlook to let you know what we think is going to happen, and try to quantify these risks. Yes, we are going hunting for Gray Swans!

Potential for Tax Reform – Gray Swan #1

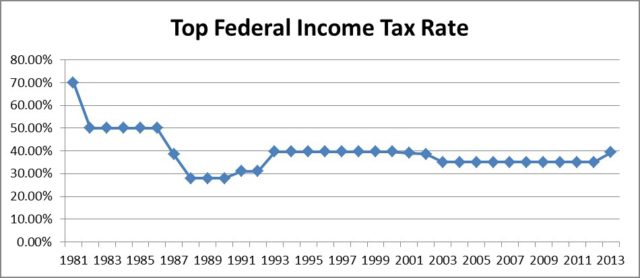

The possibility that corporate and income tax reforms could take place in 2017 is on many investors’ minds. Tax reform, historically, is considered a curse word in the muni market.

Income Tax Reform: We did a little historical analysis to see what has happened in the past when the top Federal individual income tax rate was changed. There are two recent time periods that fit well with the upcoming possible scenario:

- Tax rates went from 38.6% to 35% in 2003. The muni yield ratio with US Taxable swap rates increased 5% from 90% to 95% for 20 year maturities. This equated to a roughly 25bps underperformance in muni yields from a 4.50% 10 year benchmark.

- Tax rates went from 35% to 39.6% in 2013. The muni yield ratio with US Taxable swap rates decreased 5% from 95% to 90% for 20 year maturities. This equated to a roughly 10 bps outperformance in yields from a 1.75% 10 year benchmark.

Where are we today after the underperformance of munis following the election? JP Morgan’s research indicates the average tax rate for a municipal bond investor under Trump’s tax cut plan would go from 34% to 28%, or an estimated 26 bps of underperformance in muni yields. This seems to be on the high end of the range, given our historical analysis as we would predict 15 to 20 bps. The data from the most recent sell-off in munis (11/8/16 to 12/15/16) shows a ratio change of 95% to 100% (or a change in yields of 15 bps). The underperformance of munis has brought us to roughly a 30% tax bracket. We feel given both MainLine West and JP Morgan’s analysis, if reforms do actually happen as reported, a rational 0 to 10 more bps of underperformance is warranted. If the market reacts bigger than this, which it probably will, it is a great investment opportunity.

Corporate Tax Reform: If this takes place, it could curtail corporations’ appetite to purchase municipal bonds. This would hurt demand a bit as Corporates own roughly 16% of the municipal bonds outstanding. The bigger concern will be the impact on banks owning fewer bonds and could, therefore, further hurt liquidity in the market.

Potential for a major Infrastructure Program? Gray Swan #2

This could have a bigger influence in 2017 on the muni market than tax cuts, positive or negative, and needs to be monitored. There appears to be two possible forms of funding for a major infrastructure program that would impact munis in opposite ways.

- Trump has expressed interest in using tax credits, and having the US Government manage the program. We feel the use of tax credits is inefficient, and would be a direct competitor to tax-exempt municipal bonds, thus hurting their value.

- In DC there is an underground support to update and adjust the popular Build America Bond Program, which allows municipal localities to manage the program. We are big fans of BAB’s due to their accountability, and as they are taxable, they will draw investor money from tax-exempt investors. We feel this program could help the value of tax-exempt munis.

- The real dark horse in this race is the private sector. There is a chance that some of the projects could be funded directly by pension plans and investment firms looking for a good source of fixed income. This makes a lot of sense, but will need a strong leader to get it centralized and efficiently functioning. This could have a neutral to slightly positive effect on the muni market.

Fiscal Stimulus and its Potential Impact on Interest Rates – Gray Swan Event #3:

Muni performance will be highly dependent on your outlook for interest rates. If interest rates continue to increase, refunding supply will disappear, issuance will be roughly 75% of 2016’s, and munis will outperform. If interest rates decline, muni issuance could challenge 2016’s record high, and munis will underperform.

We feel that “secular stagnation” will continue to influence rates to stay low. There will be an attempt by the new administration to boost the economy using fiscal stimulus, but we feel there are forces in place that will limit their effectiveness. Some of these secular stagnation forces are as follows:

- Demographics in the USA and the major nations of the world. Aging and slow growing populations will restrain growth in demand.

- Demographics are slowly moving to a need for more fixed income investments as populations of the developed world continues to age. This will keep demand strong for fixed income products and help keep rates low.

- Ineffective monetary policy and the inability for the central banks to do anything to help.

- Uncertainty over future retirement funding, healthcare costs, and general fear still lingering from 2007-2008.

Potential for a Major Credit Event at the State Level – Gray Swan Event #4:

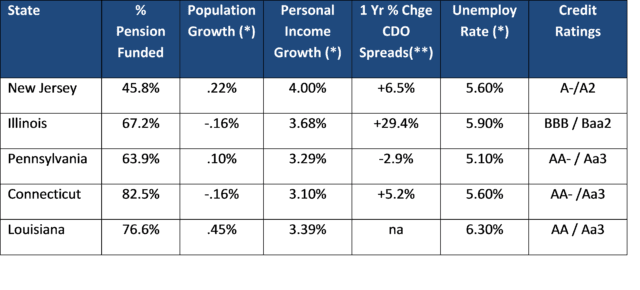

There are states that continue to struggle and their credit trends are not getting any better. Add in politics and there are a few states and one US Territory that need to be monitored.

- Virgin Islands (VI) – At year-end, S&P announced a super downgrade from BBB to BB for VI’s senior level debt. The Virgin Islands actually has more debt per capita than Puerto Rico, has a declining population, large unfunded pension balances, and a history of borrowing money to balance budget shortfalls. It appears the Puerto Rico bankruptcy process could be a road map for the Virgin Islands as it has the same problems. We recommend investors with VI exposure to review the bonds as possible sell candidates.

States that have gained more attention for their budget and credit quality struggles are listed below. If history has taught us anything about general obligation fiscal crisis, it is a slow moving process that is tied tightly to demographics. The chart below isolates some of the demographic variables for the states of recent concern. (*) 2014-2015 (**) Signifies the % increase in the probability of default from 2015 to 2016. There is no CDS market for Louisiana.

(*) 2014-2015 (**) Signifies the % increase in the probability of default from 2015 to 2016. There is no CDS market for Louisiana.

What does this tell us? Illinois is not on a good track. Concerns with the state’s general obligation pledge are warranted, and we advise a mid-term approach to reducing exposure to the state’s credit quality. This means bonds not maturing in the next five years, should be considered sale candidates when the time is appropriate.

On the positive side, is the City of Chicago back? We have been encouraged with recent developments by the City to address its budget problems, and to start shoring up its pension liability. Economically, the City is doing very well. Add in the fact that the Chicago Cubs curse is now broken. We think when the city issues bonds this year, assuming yield levels stay at 5.50% to 6.00%, it could be good high yield value. That being said, not all Chicago credits are created equal, and we recommend checking with MainLine West before going after that Chicago experience. For more information on the resurgence of Chicago, please refer to the June 2016 Monthly Credit review.

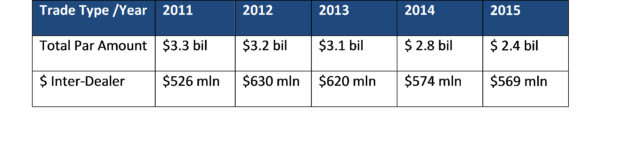

Concerns with Muni Liquidity :

Market disruptions are creating more volatility in the muni market and this is not a forecast, but a reality. Day-to-day, things are good, but when an event occurs that has a strong impact on the value of an issuer or the value of muni bonds, the market is overreacting. Why? The ability for the large underwriting banks to support the market using their balance sheet is now limited. Dodd Frank, and other recent muni regulations (price discovery), are keeping banks from stepping in and inventorying bonds like they have in the past.

A few facts that seem to back up the decline in muni market liquidity:

- The number of Broker/Dealers shrank 6.3% in 2016 versus 2015. This continues a seven-year trend of declining participation in the muni market. A lot of the decline is due to mergers and other consolidations.

What does this mean? More trading is now taking place between the final buyer and the seller. Broker/Dealers are becoming less involved with buying bonds and holding them for inventory. They simply don’t have the balance sheet freedom and profitability to do so. This means in a time of panic-driven buying and selling, investors will need to find a bid/offer from the final investor. It also means there will be issuers that could run into some liquidity problems.

This concern has us worried with the impact on the market that the Gray Swans will have in 2017. We feel any negative or positive reactions could be amplified. We would predict more 2013 taper tantrums, and 2016 Trump tantrums going forward. This can be a good thing for long-term investors whose advisors realize long-term value when it becomes available.

Navigating the Muni Market – Plans for 2017:

- Muni volatility appears to be on the rise. Gray Swans could rough up the water; we are just not sure which way they will be swimming. We recommend being nimble and ready to go with the tide depending which way they swim.

- Tax Reform will be a hot topic. We feel, at this moment, most of the “ideal Trump tax reform” is priced in. We would not sell or buy bonds now to anticipate this, but wait to see where things go. If the reforms do not take place, munis will quickly catch a strong bid.

- Corporate tax reform does not worry us regarding its impact on the muni market. However, we do think this could further pressure liquidity in our market.

- The big Gray Swan in our mind is what financing mechanism will be used for the fiscally stimulative infrastructure plan. At this time it, does not look like it will be a positive for our market as the Trump administration appears to favor tax credits. We will be monitoring our sources in DC. If BAB’s start to get some backing, and we think it is warranted, this will be a big positive for munis and increase their value. If I was given the proper odds on this right now: 10 to 1, I would take that bet!

- MainLine does not fear higher rates, going forward. Perhaps they rise a bit more, as the Fed makes its monetary moves, but “secular stagnation” and negative yields overseas we feel will keep a cap on how high interest rates can go.

- That being said, we think issuance will remain high and challenge 2016 levels.

- This will keep munis from getting too rich for too long, and allow for seasonal trading value as supply and demand technicals change.

- Credit analysis will grow in importance, especially in certain states that appear to be swimming upstream. There is value in selecting the right issuer, and the market will punish hard if you get it wrong. We also continue to prefer revenue bonds and hope to see more general obligation pledge reforms in the upcoming year like California did in late 2015 when they passed a law making its General Obligation debt top priority.

Gray Swans? Will they occur, and if they do, how will they impact munis? We do anticipate rough waters, but are not scared to set forth in 2017. We feel we have a handle on the possible events, and what we need to be looking for. Now we just need you to climb aboard and not be afraid of a Gray Swans!