The municipal bond market has seen a wave of new issuance this year, but the long-term value opportunity remains very strong. For investors, it’s important to remember the MainLine West Advantage: we focus on quality and execution, not just yield. In today’s market, it may be tempting to simply buy tax-exempt bonds with principal protection and move on, but not all bonds are created equal. The Texas Permanent School Fund (PSF), which carries the highest AAA ratings, continues to be one of the gold standards in muni finance, and MainLine looks for ways to capture that value for clients.

In August, municipal bonds delivered slight gains but remain behind on a year-to-date basis. At the start of 2025, investors faced plenty of “Red Storm” risks, but many of those clouds have begun to clear. As we move toward year-end, there is still too much value in high-quality, tax-exempt munis for the market not to correct. With stable credit quality and strong tax advantages, we believe the setup for munis looks increasingly favorable. Time for munis to correct from the “Red Storm” that seems to have passed.

Muni Market Review

Munis continue to slowly heal on the year but have yet to recover. For the month munis posted slight outperformance up .48% versus US Governments up .38% and US Corporates up .35%. On the year munis remain way behind at .32% versus 4.99% US Treasuries, and 8.02% US Corporates. Stay patient, munis may need another 30 to 60 days to turn bullish and begin playing catch up. A Fed rate cut, continued low yield volatility, and supply demand technical trends continue, is the path and things look on course.

Other August performance highlights:

- Muni yield curve steepened a bit, with yields lower from 18 to 8 bps versus taxable yields 20 to 2 bps lower.

- Year to date issuance is still up 11% from 2024, but slowly, slowing down. Still looking like a record year, but maybe lighter yearend then many thought.

- Muni demand and fund flow has been running at a somewhat stable pace, a Fed cut could spur the end of the 5% money fund parking place and a move to locking in longer-term yields.

- Tax-equivalent yields are at 15-year highs at 8.0% on the longer end for AAA-rated, closer to 8.5% for AA essential service revenue bonds.

Municipals have been the laggard in fixed income this year. Yet, with strong credit quality and their tax-exempt status intact, the value in the market looks too good to ignore. Munis began 2025 under heavy “Red Storm” clouds of concern, but much of that risk now appears to have passed. We believe it is time for a correction that could favor municipal investors.

Market News & Credit Update

- Industry Farewell: Longtime muni analyst and friend of MainLine West, Tom Doe, is stepping back from the market. Tom founded Municipal Market Analytics (MMA) in 1995 and built a respected firm by focusing on research, market trends, and distressed assets. He was also one of the first to raise awareness of climate change as a risk to muni finance. With Tom’s early guidance, MainLine now integrates climate risk into every issuer review. We thank Tom for his leadership and wish him well in his next chapter as an author.

- Natural Disaster Impact on Munis: A study from the National Bureau of Economic Research (NBER) shows that the biggest effect of natural disasters on muni bond prices occurs within three to four months after the event. Revenue bonds were most affected, with spreads widening by 54 basis points. General obligation bonds saw little impact, and the average across all bonds was 25 basis points. The study, covering 1,000 events from 2005–2018, also found outcomes vary depending on whether federal aid is provided and the wealth of the affected region.

MainLine West Tax Advantaged Opportunity Fund VIII Update:

- Tax Advantaged Opportunity Fund VIII has now made eight investments, $22 million in capital, payouts still ranging from 8.50%-10.50%. MainLine has been able to work with the underwriters to get the premium structure that fits with the Fund’s strategy and risk profile.

MW Advantage in a PSF Monsoon:

Introduction:

The Texas Permanent School Fund, or PSF, is one of the safest names in municipal finance. Created in 1983, it was designed to support Texas public and charter schools while giving investors extra confidence in school bonds. Backed by a $60 billion endowment funded through investments, oil and gas royalties, and land leases, the PSF carries the highest credit ratings available — AAA from S&P and Aaa from Moody’s. When a bond is guaranteed by the PSF, it means the fund stands behind the repayment of that debt. For schools, this lowers borrowing costs. For investors, it provides stronger protection of principal and a high level of security. Today, the PSF guarantees more than $130 billion of bonds, making it one of the most trusted programs in the municipal market.

Why so much issuance?

Just in the month of July and August, roughly 120 districts borrowed over $12 billion tax-exempt, predominantly long-term bonds. For the year, PSF issuance is on track to surpass the previous record set in 2024.

Year | Total Par (billions) | # Deals |

2020 | $8.6 | 231 |

2021 | $3.5 | 86 |

2022 | $15.0 | 225 |

2023 | $17.7 | 216 |

2024 | $21.6 | 287 |

2025 – Year-to-Date | $21.3 | 200 |

This summer’s rush to issue is driven by a Texas House Bill that, if passed, would take effect on September 1st and prohibit the use of PSF insurance by issuers. It would not impact the current bonds outstanding. This has a very remote chance of passing, but issuers prefer to be safe than sorry.

Why PSF?

Strong Credit Quality – PSF-backed bonds come with an exceptional track record – there has never been a default by an underlying issuer. Many of these school districts are financially strong on their own and carry a full faith and credit pledge. In addition, issuers must meet strict criteria to qualify for the PSF guarantee.

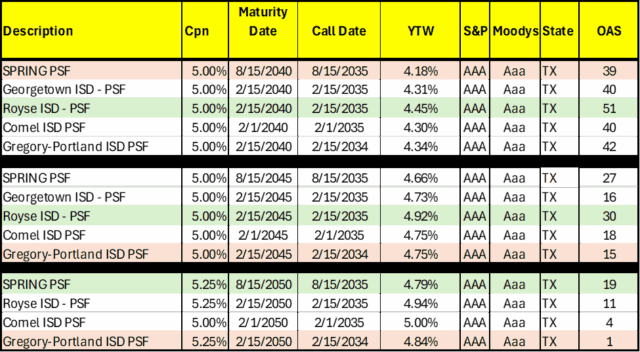

Attractive Income – PSF bonds often trade at a spread above comparable index bonds. Right now, with heavy new issuance in the market, they are trading at even more attractive levels. MainLine reviewed five recent PSF-backed deals to evaluate the value offered and to see whether pricing was consistent across issuers with different credit profiles.

Analysis – Are all PSF bonds the same?

We wanted to test how the market values the PSF guarantee. Do all PSF AAA-backed bonds trade the same, or do weaker underlying issuers have to offer higher yields? To find out, MainLine analyzed five new issues and compared their option-adjusted spreads (OAS), which measure credit risk after adjusting for call features. In theory, if all PSF guarantees were viewed equally, OAS levels across issuers should be similar. But if investors factor in underlying credit quality, weaker school districts should trade at wider spreads than stronger ones.

Below is a chart comparing different issuers at different parts of the yield curve. The issuers are ranked by our credit profile score from strongest to weakest, the cheapest priced are highlighted in green, richest in orange:

As the analysis shows, the muni market seems to ignore the underlying credit rating but also does not look at every PSF deal as the same (i.e. range of OAS’s). Other factors that may have influenced the results have to do with the size of the issuer (the bigger the better) and the underwriter (the bigger the better). Royse ISD (cheapest in 2 of the maturities) was the smallest deal and managed by the smallest underwriting firm. Why is MainLine worried about the OAS and which is cheaper? The additional risk/return trade off buying the higher OAS (51 vs 39) can add 12 more bps of annual income ($1,200 per $1 million par). Over ten years this becomes $12,000 in income and over thirty years it grows to $36,000.

Conclusion:

What does this mean for you? While every PSF-backed bond offers strong principal protection, not all of them provide the same level of income. That is where MainLine comes in. We navigate the fine print to help maximize your tax-exempt income. Even with AAA-rated PSF bonds, our careful management of the details can result in an extra $1,200 of income each year for our clients.