Review of 2025 Muni Market

2025 was quite a year for Munis, especially if you viewed it as an opportunity. The “Red Storm” following the 2024 Election brought a series of risks to the Muni market. Some were legitimate, others were noise. In the end, the for-the-public-good market reaffirmed its essential role in financing US infrastructure and is now positioned to play an even larger role within the broader financial markets. MainLine West reviews its 2025 Outlook and examines the actual impact the Red Storm had on Munis.

In November, munis paused with slight underperformance, and that may be enough to limit the possibility of a full fourth quarter comeback. MainLine still expects a constructive finish to the year and a strong start to 2026, but recovering the remaining 2.52% year-to-date return gap would make December a month to remember.

Muni Market Review

Munis softened in November after two months of outperformance, with a monthly return of 0.23 percent (Bloomberg Muni Composite Index) versus 0.62 percent for US Treasuries and 0.65 percent for US Corporates. Year to date, Munis remain behind at 4.15 percent compared with 6.67 percent for US Treasuries and 7.99 percent for US Corporates.

December looks favorable. Supply and demand technicals remain supportive, Munis offer relative value, and the Muni fear index is near historic lows. Additional November highlights:

- The Muni yield curve flattened, with yields higher by 4 to 1 bps, while the taxable curve steepened with yields ranging from down 7 to up 1 bps.

- Year to date issuance is up 12.8 percent from 2024 and has already reached a new annual record. Munis handled the heavier supply better in recent months as fund inflows were positive until late November.

- After reaching its steepest level ever, the Muni yield curve has begun to normalize, with longer maturities outperforming. The curve remains extremely steep between 15 and 20 years. The traditional 80/50 income strategy now resembles a 90/50, meaning an investor can earn 90 percent of the income of 30-year Munis while taking only half the price risk.

MainLine is looking for a strong year-end for Munis, but can they make up the current year-to-date return difference of 252 bps? If so, December will be a month to remember. The weak month of November may have cost Munis a fourth quarter comeback.

MainLine estimates the Tax Advantaged Opportunity Funds’ NAVs were down 1 to 2 percent for the month, reflecting the slight underperformance of Munis. The funding rate has remained roughly 65% of the swaps floating rate, keeping cash payout steady through the Muni comeback bid.

Market News & Credit Update

- The AI boom is now influencing the Muni market. A Barclays research report highlights how AI has sharply increased the demand for power and infrastructure, placing pressure on supply and requiring the construction of new capacity. Utilities with older plants, limited fuel diversity, and lower wealth service regions will face the greatest credit stress. Wealthier regions and utilities with newer, diversified power sources will be less affected. While some negative credit implications are expected, MainLine believes the impact will be modest because electricity is an essential service and political intervention is likely. Consumers, however, will face higher costs as the grid adapts to support artificial intelligence.

- Issuance surpassed 535 billion dollars in early November across 8,425 deals, breaking last year’s $513 billion total with nearly two months left. Analysts expect 2025 to finish near $560 billion. Early 2026 projections are similar. At this pace, the Muni market, which hit 4 trillion dollars in 2021, is on track to reach 5 trillion dollars by 2027 or 2028. The growth reinforces the expanding importance of tax-exempt financing for national infrastructure.

Red Dawn Setting – White SWAN Rising?

Review of Muni Market 2025

MainLine started the year with its Outlook for 2025 as follows:

There have been numerous “defining” Muni market moments over the years, some good and some bad. Two of the top five events would have to be the Tax Reform Act of 1986 and the Meredith Whitney call for the financial demise of major cities in 2010. One event was bad for Munis, while the other was good. In each case, the story came down to the “news” versus the reality behind it. You could call them “once in a twenty-year Muni opportunity (or disaster).”

MainLine views the change in political leadership in the United States following the 2024 election as one of these potential moments. Opportunity? Disaster? Will the rise of the “red dawn” bring an end to the “for the public good” White SWAN market, or will it be a beautiful sight for SWAN investors?

So how did we do? Let’s take a quick look back at the last eleven months in Muni-land.

Review of Red Storm Risks in 2025:

MainLine began 2025 with a set of concerns about the Red Storm and its impact on Munis. Looking back, here is how those risks unfolded:

Tax rate reductions: MainLine expected the 2017 tax cuts to be extended, keeping the top tax rate at 37% going forward. That extension turned out to be the only attempt in 2025 to reduce tax rates. Some analysts expected an additional round of cuts after the extension, but that never materialized. In the end, the Red Storm worry had no real effect on the municipal market. Tax-exempt bonds continued on as business as usual.

Restriction of tax-exempt status for select issuers: MainLine anticipated the possibility that some Muni sectors will no longer have the ability to issue tax-exempt debt. We thought sectors such as healthcare, higher education, and transportation (ports, airports) were possible candidates. Higher education became ground zero for the Red Storm as there has been attempts to take the nonpublic status away from higher education institutes. This set off a rush to issue bonds by the sector, which then got the attention of other sectors that became worried. This was the biggest Red Storm risk to impact the Muni market in 2025. Muni supply is set to hit a new record and was front loaded in the first half of the year. This additional issuance has taken time for the market to absorb and has been a key factor in Muni underperformance.

Loss of tax-exempt status: MainLine initially expected there could be serious discussion about municipalities losing their tax-exempt status as a way to help cover the cost of extending the 2017 tax cuts and funding other Red Storm policies. This idea circulated during the first few months of the year but was quickly shut down by Muni advocates and now seems like a distant memory. Perhaps Washington DC has finally recognized the long-term value of tax-exempt financing – something we have emphasized here for years.

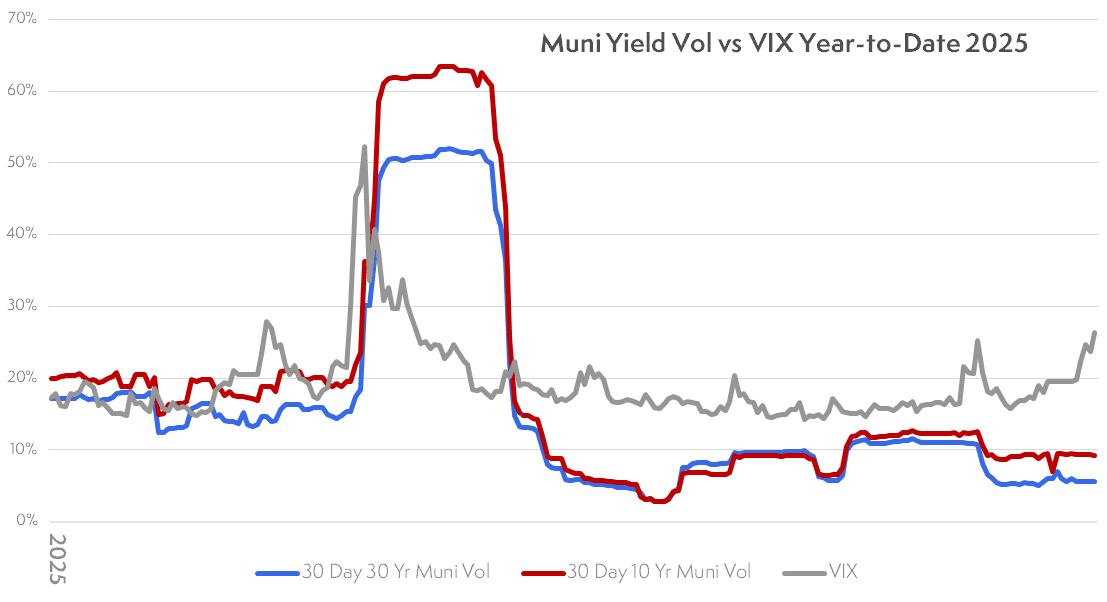

Muni Fear Index Review:

The Red Storm caused a sharp spike in the Muni fear index, and combined with heavy supply, it weakened demand, especially for maturities beyond 10 years. As 2025 progressed, the fear index moved back to more constructive levels, which helped drive the recent outperformance of Munis heading into year end.

Below is a chart showing the Muni fear indices for the year.

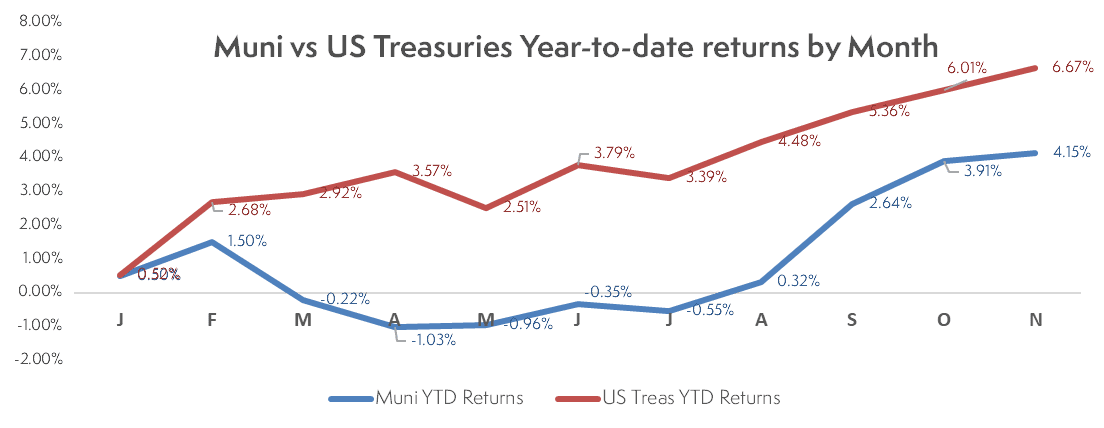

Muni Returns in 2025:

MainLine anticipated the market would struggle early in the year and then eventually recover. This would create a buying opportunity. True to our word, MainLine executed Fund VIII in the height of Muni underperformance. Unfortunately, Munis have not fully recovered yet, but are on their way with good momentum going into 2026. Yes, this may be a clue into our 2026 Annual Outlook we will release in early January.

Below is a year-to-date chart of the cumulative Muni returns versus US Treasuries by month.

At their lowest point on April 30, 2025, munis were down 1.03% while US Treasuries were up 3.57%, a gap of 4.60%. By the end of November, that gap had narrowed to 2.52%, with munis up 4.15% and Treasuries up 6.67%.

The question now: Can munis complete the comeback, maybe even pull off a Denver Broncos fourth quarter rally to win?

Conclusion:

As we move from 2025 into 2026, MainLine believes the “Red Storm” has finally passed. The For-the-Public-Good sector has shown just how essential it is to U.S. infrastructure, and we think it’s now positioned to play a much bigger role in the broader financial markets.

The market turbulence we expected ultimately created what MainLine views as one of the top five buying opportunities in municipal bonds in recent memory, especially for investors who:

- Bought bonds during peak volatility and locked in 15-year high tax- equivalent yields exceeding 8 percent.

- Invested in Fund VIII and secured a 9+ percent tax-exempt payout for years to come.

2025 demonstrated that uncertainty creates fear, and fear creates opportunity. Muni investors had the chance to deploy capital and now sail out of the Red Storm into calmer waters.

MainLine calls that “Muni Serenity”.