Municipal bonds continue to offer investors reliable, tax-advantaged income, yet their performance remains closely tied to shifts in the broader economy. For this month’s review, Portfolio Manager Mike Maciolek has passed the pen to MainLine’s Head Trader, Paul Dannenhauer. He highlights three major forces currently shaping the muni market: Federal Reserve interest rate policy, inflation dynamics, and the connection between economic growth and local tax revenues.

Muni Market Review

Munis continue to recover gradually this year but have not yet fully rebounded. For the month, munis posted slight outperformance, up 0.48% versus U.S. Governments at 0.38% and U.S. Corporates at 0.35%. Year-to-date, munis remain behind at 0.32% compared to 4.99% for U.S. Treasuries and 8.02% for U.S. Corporates. Stay patient—munis may need another 30 to 60 days to turn bullish and begin playing catch-up. A Fed rate cut, continued low yield volatility, and stable supply-demand technicals all suggest the market remains on course.

Other August performance highlights:

- The muni yield curve steepened slightly, with yields down 18 to 8 bps, versus taxable yields down 20 to 2 bps.

- Year-to-date issuance is up 11% from 2024, though slowing. While still on track for a record year, totals may be lighter by year-end than previously thought.

- Muni demand and fund flows remain steady. A Fed cut could shift money away from 5% money market funds and into longer-term yields.

- Tax-equivalent yields are at 15-year highs: about 8.0% on the long end for AAA-rated bonds and closer to 8.5% for AA-rated essential service revenue bonds.

Municipals have trailed other areas of fixed income this year, but their strong credit quality and tax-exempt status continue to stand out. While 2025 began under a cloud of uncertainty amid the “Red Storm”, many of those risks have since eased. With attractive valuations now in place, we believe conditions are lining up for a potential rebound that could favor municipal investors.

Market News & Credit Update

- Florida’s proposal to eliminate property taxes appears more political theater than reality. Still, it raises questions about the lengths a “red” state government might go to create fiscal challenges for its “blue” localities. In Florida, of the top five cities in terms of population, four of them have Democratic mayors. Property tax provides over $55 billion in annual income for local governments, which is used for education, healthcare and public safety. Its elimination would have a dramatic negative impact on providing these services and the fiscal health of counties and cities in Florida. A proposal to replace property taxes with a state sales tax would increase it to 12%, the highest in the nation and would be very regressive on lower and middle-income residents. So why are Florida legislators meeting and studying this? It is nothing more than the State’s way to audit its localities, throw political punches at them and make an investor wonder how far politics can impact public finance? MainLine is not saying that there may be room for property tax reforms, but if Florida truly wants to lower property taxes, they can introduce an income tax. Ultimately, the revenue must come from somewhere, whether the “front pocket” or the “back pocket,” taxpayers still foot the bill.

- Muni new issuance is growing, and MainLine believes it has only just begun. By mid-September, new bond sales topped $400 billion – once considered a full year’s issuance. Analysts now estimate 2025 could set a record near $550 billion, with $600 billion possible as early as 2026. Slower economic growth and softening revenues, combined with persistent infrastructure needs, will likely continue, driving issuance higher.

The Macro Balancing Act: Key Drivers of Today’s Muni Market

The municipal bond market continues to be shaped by three core forces: Federal Reserve policy, inflation trends, and economic growth’s impact on tax revenues. Together, they determine how attractive munis look compared to other fixed income investments.

Federal Reserve Decisions & Yields

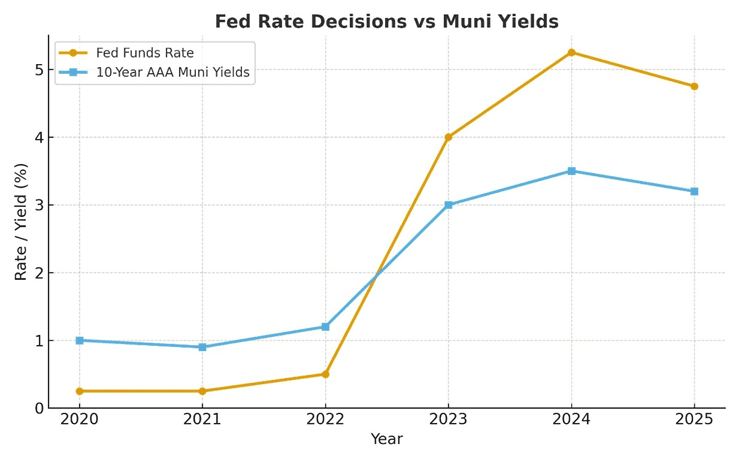

The Federal Reserve’s rate policy is one of the most important drivers of municipal yields. When the Fed raises rates, muni yields generally rise as well, pressuring prices but creating new opportunities for buyers seeking higher income. Conversely, when the Fed signals a pause or cut, muni yields often decline, pushing prices higher.

The chart above shows the relationship between Fed Funds Rate and 10-Year AAA Muni Yields. It highlights how Fed policy moves have historically influenced muni yields — when the Fed holds rates higher, muni yields tend to rise as well, impacting both investor returns and issuer borrowing costs.

The Fed’s recent “higher for longer” stance has put upward pressure on yields across the fixed-income space. For muni investors, this creates a window to lock in historically attractive tax-exempt income, though issuers face higher borrowing costs. The path forward depends heavily on how soon the Fed feels comfortable easing policy.

Inflation’s Impact on Demand

Inflation has a unique and often two-sided effect on municipal bonds. When consumer prices rise quickly, the fixed coupon payments offered by munis lose some of their real value, leading many investors to demand higher yields as compensation. This dynamic can temporarily pressure muni prices lower. Conversely, when inflation begins to cool, munis tend to look more attractive—particularly to high-income households who value the combination of stability and tax-free income. Importantly, municipal revenues are often tied to property, sales, or income taxes, which can actually rise with inflation, helping strengthen the credit profile of many issuers.

Today, inflation has moderated significantly from the peaks of the last cycle, though it still sits above the Federal Reserve’s long-term 2% target. For muni investors, this trend is encouraging: purchasing power erosion is less of a concern, issuer credit conditions remain healthy, and steady demand for tax-exempt bonds should continue to support the market.

Economic Growth and Tax Revenues

The health of the economy flows directly into municipal credit quality. Stronger employment, rising wages, and higher property values all boost income, sales, and property tax revenues. This supports governments’ ability to service debt and maintain fiscal flexibility. Conversely, weaker growth softens collections and exposes vulnerabilities, especially in regions reliant on narrow revenue sources.

Currently, tax revenues remain solid thanks to resilient job growth, consumer spending, and property values. This reduces the likelihood of service cuts or tax hikes, both positives for bondholders. However, risks vary by region: areas facing slower growth, industrial concentration, or population decline may see fiscal stress sooner than diversified, growing regions.

Bottom Line for Investors

Today’s muni market offers both challenges and opportunities. Elevated yields provide compelling long-term value, while inflation is trending lower and tax revenues remain healthy. Credit fundamentals are sound, but careful issuer selection remains important.

Conclusion

The muni market is being shaped by three key forces: Fed policy, inflation trends, and economic growth. Together, they create a market environment where attractive yields and solid credit quality offer a strong backdrop for long-term investors. For retail investors, that balance currently tilts in favor of opportunity, with attractive yields and strong credit quality providing a solid backdrop heading into year-end.