Opportunity is Knocking – GRVIII! (Great 8)

Does a SWAN (Sleep-Well-At-Night) investment strategy that offers equity-like returns sound like a good opportunity? How about a fund strategy that delivers tax-exempt income with equity-like performance? That sounds like a great opportunity. Municipals are offering tax-equivalent yields near 15-year highs, maintaining top-tier credit quality, and remain MainLine West’s singular focus.

It’s been another month of weak municipal performance, but the theme is familiar: heavy supply and lingering uncertainty—though both are finally starting to ease. MainLine believes munis may stage a come-from-behind rally in the final quarter of 2025, potentially matching the returns of other fixed income sectors. With tax-equivalent yields near all-time highs, the muni fear index at all-time lows, and the yield curve at record steepness, we may be headed for an all-time photo finish.

Muni Market Review

June was yet another month of weak muni performance. Munis were up .10% trailing US Treasuries at .36%, and US Corporates at .48% (Bloomberg composite indices). It remains the same old muni theme, high supply, and uncertainty which has begun to decline. MainLine feels things are lining up for a good final lap in 2025. Can munis catch up in the final quarter of the year? More June highlights were as follows:

- Muni yield curve steepened during the month with the short end 27 bps lower and the long-end 11 bps higher. The curve is now at record steepness (128 bps). This reflects retail’s fear with investing any longer than 10 years.

- Taxable yields were lower by roughly 22 bps on the month along the curve.

- Munis are cheap 10 years and out relative to taxables. The further out the curve you go, the better the value.

- Year to date issuance is up 13% from 2024, and 25% versus the five-year average. Higher education issuance is up 60% and school districts up 40% for the year. These remain the big drivers to the record supply over 2024.

- The muni fear index went from all time highs in April to all time lows in June. MainLine expects this to help drive higher inflows going forward, which will help increase demand.

MainLine remains focused on launching Fund VIII. The opportunity is compelling, and if you’re interested, we encourage you to reach out as soon as possible.

Market News & Credit Update

- U.S. state budgets are feeling the pressure from Trump-era and Department of Energy policy shifts. States are warning of significant revenue losses due to federal cuts and trade-related policies. This comes at a time when revenues are flat, and inflation is driving up infrastructure costs—forcing many states to issue more debt. For example, Maryland estimates a $350 million loss, which recently led to a downgrade from Aaa to Aa1 by Moody’s.

- U.S. public transit authorities are still suffering from the lingering effects of the COVID-19 pandemic. Ridership has not returned to pre-pandemic levels, and major cities’ transit systems continue to face fiscal shortfalls. Transit systems serving San Francisco, Washington D.C., Chicago, Philadelphia, and Boston are all experiencing financial strain and the potential for credit rating downgrades. These agencies now face difficult choices: raise fares, lay off workers, or cut service to address the fiscal imbalance, as the anticipated rebound in ridership has not materialized.

GR VIII – Opportunity is knocking

Background:

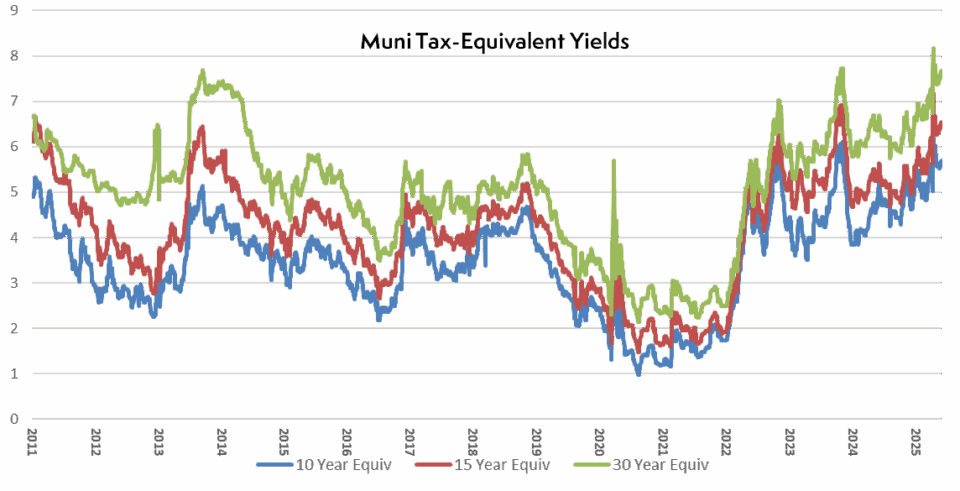

The combination of high rates, and muni cheapness from record supply and political and market uncertainties has pushed tax-exempt rates up to their best values since 2011 and 2013. Below is a chart showing the AAA-index yields for muni bonds maturing in ten, fifteen, and thirty years. Tax-exempt yields are grossed up by top federal tax rate of 37%, and Medicare tax rate of 3.8%.

Introduction:

At close to 8%, muni tax-equivalent yields are at a 15-year high and lock in a winning long-term sleep-well-at-night investment opportunity. This is not an opportunity that comes along often and investors should seriously consider increasing their municipal exposure, or getting started with one. MainLine has two ways to answer this opportunity:

- SMA- separately Managed Accounts

- Tax Advantaged Opportunity Fund VIII – GRVIII (Great 8!)

Why SMAs?

- Customized strategies that focus on intrinsic muni value, executed to minimize costs and maximize tax exempt income, federal and state.

- At this moment, MainLine could execute the following SMA strategies:

Managed Duration 2.80%-2.90% Tax Equivalent 4.75-4.90%:

A short-term strategy designed to take pick up yield without compromising expected proceeds risk and maintains low-pricing risk. Income is derived by using “cushion bonds” and bonds with sinking funds and prepayments – all designed to trade close to par, but pick up income due to the expected proceeds reinvestment risk that can be rolled back into this strategy.

80/50 4.20%- 4.30% Tax Equivalent 7.10%-7.30%:

The 80/50 is an intermediate term value driven investment strategy designed to take advantage of the income benefits inherent in the slope of the yield curve (80% of the curve’s maximum yield) and the defensive structural benefits of premium callable bonds (50% of the price risk). Strategy is designed to maximize tax-exempt income without the risk of long duration pricing risk.

Max Yield Strategy 4.75%-4.85%, Tax Equivalent 8.00%-8.20% :

A long-term strategy designed to maximize tax-exempt income and build wealth without regard to pricing risk. Max yield is for the investor making a long-term commitment to the principal-first tax-equivalent top-tier performing municipal bond market. This strategy looks to pick up income by investing out on the curve, as call/extension risk is mispriced, given the history that most bonds are called prior to their maturity dates, yet investors earn the additional income from the curve.

These yields do not consider the state tax exemption which would push the tax-equivalent yields even higher for each of the strategies: SWAN investment strategies with equity-type returns.

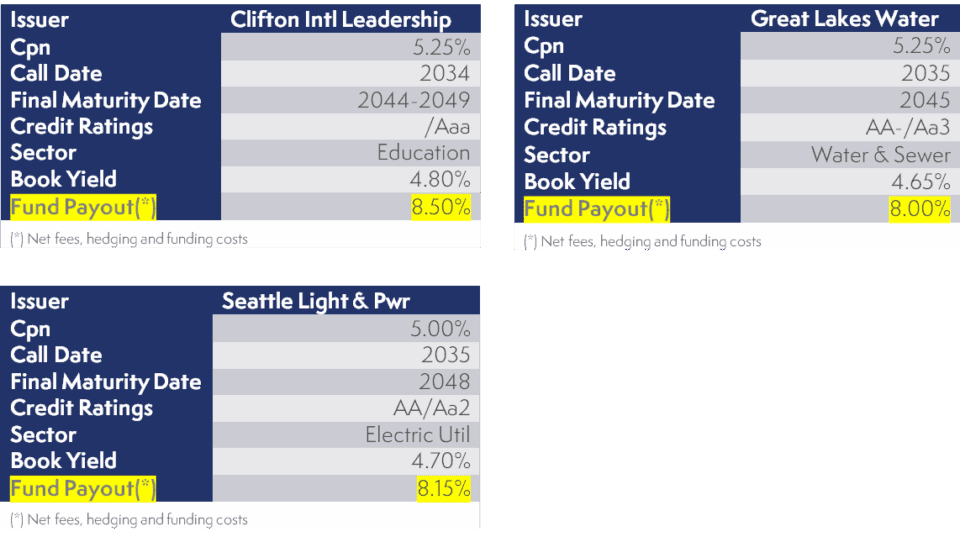

All the bonds in these examples are essential-service revenue bonds, with credit ratings of AA or higher and from issuers with good underlying demographics. The tax-equivalent payouts of 13.5% to 14.4%, which more than rewards investors for an illiquid five-to-seven-year commitment.

Conclusions

Long -term stock performance has historically been around 8% to 8.50% and is taxable. Municipal strategies that can equal (or beat) stocks represent a great opportunity:

- SMAs paying out 8%-8.20% tax-equivalent. A SWAN investment strategy that matches equity returns.

- A Fund strategy that pays out 8.0-8.50% tax-exempt that equals 13.5% to 14.4% tax-equivalent. This far outperforms equity returns.

Are these great opportunities?

Yes – GRVIII!