There are some things in life we know to be certain: the sun rises in the east and sets in the west, two plus two equals four, and if the top income tax rate goes down, munis—and the value of tax-exempt income—go down. Or do they?

Munis once again underperformed, declining in value while other fixed income assets held steady or gained. A record level of issuance and increased yield volatility has created an imbalance between supply and demand, resulting in higher yields. The good news: tax-equivalent yields are attractive—8.25% for intermediate-term and 9.25% for long-term bonds—and technicals are expected to turn positive as we move through May.

Muni Market Review

Munis continue to disappoint and once again underperformed for the month. The good news is that MainLine believes this trend is nearing an end, as yields are now very attractive and technicals are expected to improve through May—and even more so in June and July. Record issuance and historically high volatility have led to reduced demand and have munis on the defensive.

For the month the Bloomberg muni composite was down .81%, US Treasuries up .63%, and US Corporates down -.03%. More April highlights are as follows:

- Muni yields were higher by 16 to 14 bps, with taxables lower from 15 to 2 bps.

- Housing bonds and Prerefunded bonds were top performers, hospitals and electric utilities were the worst performers.

- Year to date issuance is up 25% from 2024, led by higher education and airport issuance.

- Muni yield volatility is at the highest on record since 2020 COVID. Current muni yield volatility is at 70%, this is versus 18% for 2023 and 2024. MainLine believes high volatility creates investing fear for retail muni investors which causes outflows and apprehensiveness to buy new bonds.

MainLine believes munis are poised to change course and should perform well over the next 60 to 90 days. Strong technicals and attractive yields may finally get the muni market back on track.

Market News & Credit Update

- MainLine is monitoring speculation that Congress may change the tax-exempt status of municipal bond interest to a capped deduction at 28%. While less drastic than eliminating muni tax benefits entirely, this change would still negatively impact muni valuations. MainLine estimates it could lower prices by 50 to 75 basis points. For example, a $1 million, 15-year bond could lose $65,000 in value. For investors holding to maturity, this wouldn’t affect the return of principal or the yield earned. However, it would increase borrowing costs for municipalities—costs ultimately passed on to taxpayers. MainLine sees little justification for such a move.

- MainLine preaches investing in bonds for essential services, but there are also nonessential service bonds, that are a bit entertaining and add a little excitement to our SWAN world. In April $300 million in tax-exempt bonds yielding 7% were sold to fund the “The Shining Experience” . The proceeds will be used to renovate, build a new event center, and add on 65 new rooms to the Stanley Hotel in Estes Park, Colorado. The event center will be dedicated to the legendary horror movie and revenues from the hotel will be used to repay the bonds. They are non-rated, leaving MainLine with one question, is there a redrum?

MainLine West Family of Funds Update:

Fortunately, with volatility comes opportunity. This leads us to the imminent launch of MainLine West Tax Advantaged Opportunity Fund VIII.

We are currently soliciting investor interest in Fund VIII.

Unlike high-yield muni bond strategies, to which we are usually compared, our approach is an arbitrage between high-quality municipal bonds and high-quality taxable bonds.

We patiently wait to deploy capital until the relationship between tax-exempt and taxable bonds demonstrates relative value.

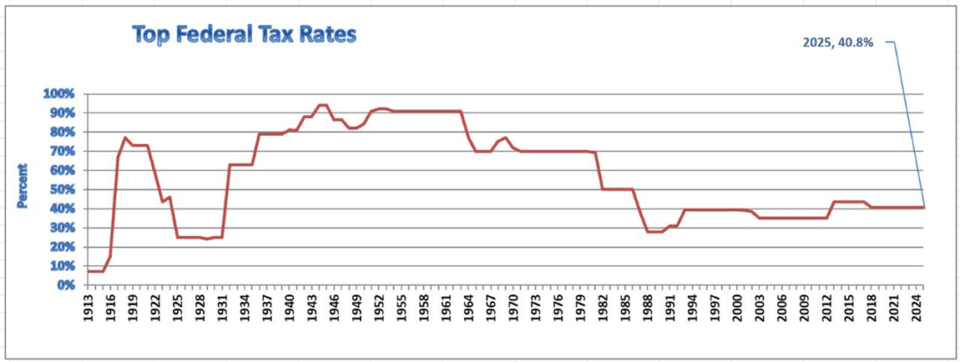

Since 1961, maxing out at 90%, tax rates have been on the decline. The tax cut of 1961 from 90% to 70% is before muni market pricing information is available. This leaves us with analyzing the tax acts of 1981, and 1986. This monthly will focus on what happened to tax rates, and how did the cuts impact the municipal market.

Tax Reform Act of 1981

The Kemp-Roth Tax Cut was an act that cut the highest marginal tax rate from 70% to 50%, and the lowest tax bracket went from 14% to 11%. The cut was designed to encourage economic growth during President Ronald Reagan’s first term. This act also reduced estate taxes, capital gains taxes and corporate taxes, most of which were reversed in 1982.

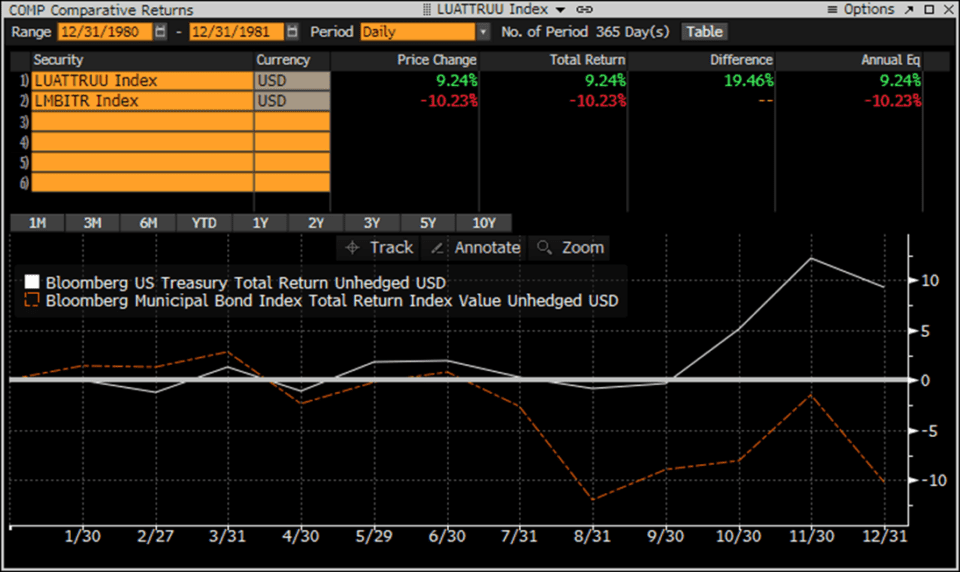

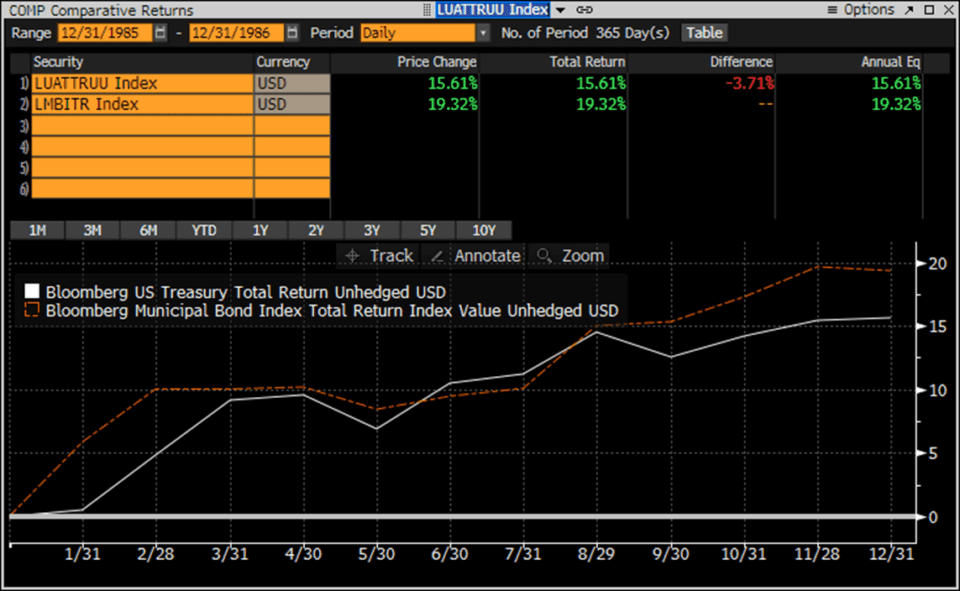

Below is a graph showing the return of the Bloomberg Composite Municipal Bond Index (red line) versus the Bloomberg US Treasury Composite Bond Index (white line).

This 20% decrease in top tax rate, decreased the value of tax-exempt income and the municipal market underperformed.

- Muni Bloomberg Composite index was down 10.23% for the year

- US Treasury Composite Index was up 9.24%.

A cut in the top tax rate, hurting the value of tax-exempt income. Some things we know are still certain!

Tax Reform Act of 1986

On October 22, 1986, for the first time ever, President Reagan signed into law a tax reform policy that lowered the highest tax rate, while increasing the lowest tax rate.

The 1986 Tax act lowered the top tax rate from 50% to 28%, while raising the bottom tax bracket from 11% to 15%. Other than just the tax rate, this act also changed the tax playing field as follows:

- Eliminated the distinction between long-term capital gains and ordinary income.

- It mandated that capital gains be taxed as the same rate as ordinary income raising maximum tax rate on long-term capital gains to 28% from 20%.

- It restricted tax benefits for certain types of bonds and disallowed financial institutions from deducting interest paid on debt to carry tax-exempt securities. This stopped banks and other investors from borrowing and buying munis, ending a very easy and safe arbitrage opportunity.

- Reduced the types of private activities that could be financed with tax-exempt bonds. This reduced some of the supply in munis.

- Capped the amount of industry development bonds (IDB), which also reduced the supply of munis.

- Eliminated corporates from owning munis, causing them to buy bonds all through 1986 as the tax-exempt income would be grandfathered going forward.

- Other loopholes to avoid taxes were closed, leaving the wealthy with fewer ways to generate more tax exempt income.

The 32 % decrease in the top tax rate caused munis to slightly outperformed.

- Muni Bloomberg Composite index was up 19.32% for the year

- US Treasury Composite Index was up 15.61%

What? Why? Doesn’t a lower top tax rate hurt the value of tax-exempt income? Well, it’s not that easy, the Tax Act of 1986 changed a lot of things and in the end munis prevailed. Here are a few theories as to why:

- The supply of new bonds was decreased with the elimination of private activity and IDBs.

- Demand from wealthy individuals and institutions remained strong, as other tax shelters were eliminated.

- Much of the impact was already priced in, as it took years for the tax act to finally become law.

- Munis still offered compelling risk-adjusted tax equivalent returns versus other investments.

Conclusion:

One thing remains certain: recent and potential tax reforms are contributing to a higher implied tax rate in the long end of the municipal curve. Currently, municipal bonds as a percentage of taxable yields stand at about 95% for 30-year maturities, compared to 75% for 5-year maturities. This spread, in addition to credit risk, reflects the uncertainty surrounding top marginal tax rates over the next three decades. The possibility of future tax cuts must be priced into long-term muni yields to ensure investors are adequately compensated for this risk.

The “Red Storm” of 2025 signals the potential for broad changes in tax policy, municipal bond regulation, and economic direction. As this period of uncertainty plays out, the municipal market could evolve in several ways. Despite the challenges, MainLine remains confident that bonds issued for essential public services—supporting municipalities of all sizes—will weather the storm and emerge stronger and more valuable than before.