2025 arrived with force, bringing multiple “red wave” threats from Washington that unsettled the municipal bond market. Yet, as the year closed, municipals were sitting calmly in a tranquil pond, more beautiful than ever. Year-end trading was the quietest MainLine can remember in terms of yield volatility and market activity. The uncertainty and turbulence that dominated much of 2025 appeared to fade away. Could the runt of markets finally earn respect from politicians and investment advisors? Could the “sleep well at night” market finally find serenity?

Much of 2025 was spent worrying about the potential dismantling of the municipal market through the loss of tax-exempt status and declining values. In hindsight, MainLine believes 2025 laid the groundwork for a stronger and more resilient municipal market. Not only did issuance reach record levels, but new sectors emerged, the market reaffirmed its value to the public good, and municipals continued to evolve as an asset class.

Introduction:

Serenity is defined as a state of calm and peacefulness. It is remarkable that the municipal market, once threatened by political disruption and shaken by a summer of record tax-equivalent yields, could enter 2026 in such a composed position.

What does “serenity” mean for municipals in 2026? MainLine believes the market is set up for a year of calm, steady returns. Municipals will continue to evolve technically, operationally, and in their importance to U.S. capital markets. Simply put, 2026 is about bigger and better municipals.

2026 Outlook Highlights:

- The Muni march to $5 trillion – Supply continues to grow.

- The continued commoditization of the Muni market

- Munis and the affordable housing crisis

- Munis & AI, partners on and off the field

- Credit Quality trend is turning down, but remains strong

The Muni March to $5 Trillion – Supply Continues to Grow

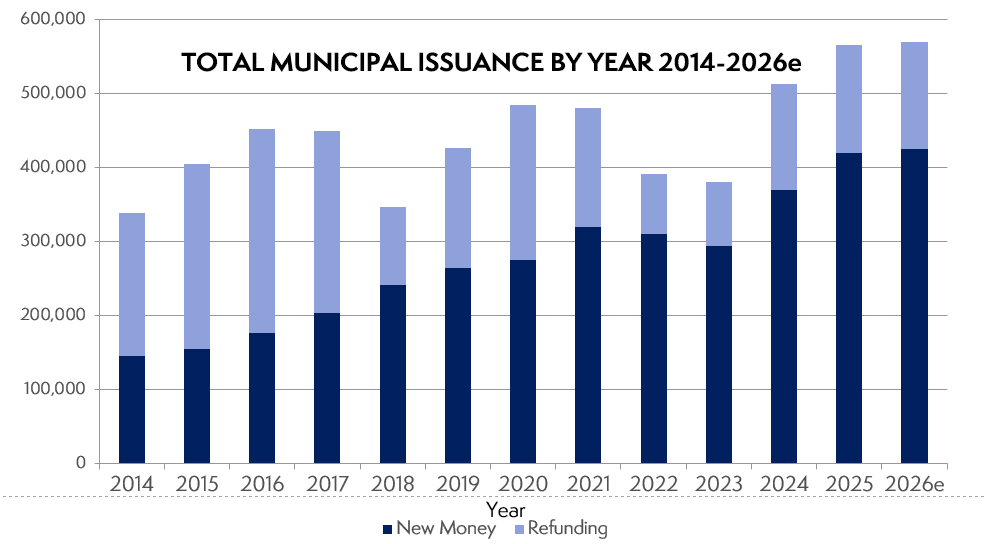

Supply in 2025 appears to have set a new record at approximately $565 billion, surpassing the prior record of $513 billion in 2024. Analysts forecast annual issuance between $520 billion and $575 billion going forward. MainLine believes 2026 will again set a record, with supply closer to $570 billion.

- Why does MainLine expect continued growth?

- Costs for projects have increased

- Federal infrastructure aid tied to COVID has ended

- State and local budgets are tightening, pushing issuers toward debt rather than revenues

- New sectors emerged in 2025, including spaceports and data centers. Data centers, in particular, will drive additional issuance to finance water and electric infrastructure

At this pace, what became a $4 trillion market in 2021 could reach $5 trillion by 2028. Even then, municipals remain relatively small compared to other U.S. markets: approximately $30 trillion in U.S. Treasuries, $11 trillion in corporate bonds, and $70 trillion in equities.

This rapid growth has weighed on returns in 2024 and 2025. The trend will again test the market in 2026, as estimated net new supply (new issuance minus coupons and maturities) is forecast to range from flat to $50 billion. For municipals to absorb this supply and outperform, demand must grow.

Where does the extra demand come in 2026?

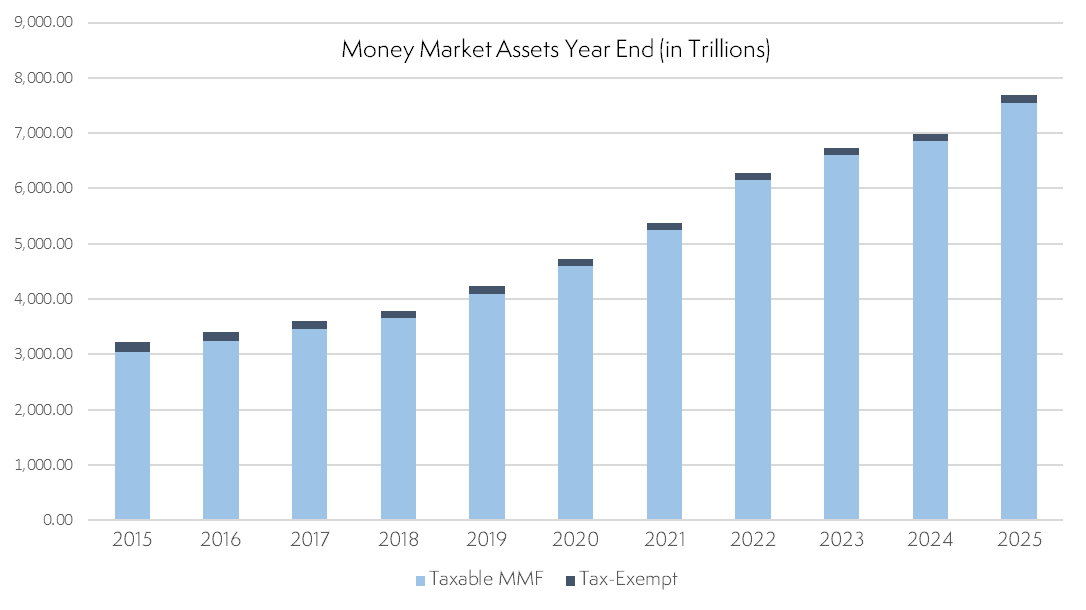

- Reallocation from money market funds to fixed income. Since early 2025, money market yields have fallen from about 5 percent to roughly 3.7 percent, a decline of more than 25 percent in income. Investors can still purchase a 10-year municipal bond yielding around 3 percent, which equates to approximately 5 percent on a tax-equivalent basis. Further declines in money market yields are expected as the Fed eases policy, potentially pushing yields closer to 3 percent by year-end.

- New investor structures. Morgan Stanley sees potential demand from pairing less liquid, tax-advantaged alternative investments with more liquid, tax-exempt municipal bonds.

- Growth of SMAs and ETFs. Investment firms continue to make municipals easier and more cost-effective to own, attracting new buyers.

- Improved confidence. Underperformance in 2025 and reduced policy uncertainty from Washington should help rebuild investor confidence. This trend is reflected in MainLine’s Fear Index.

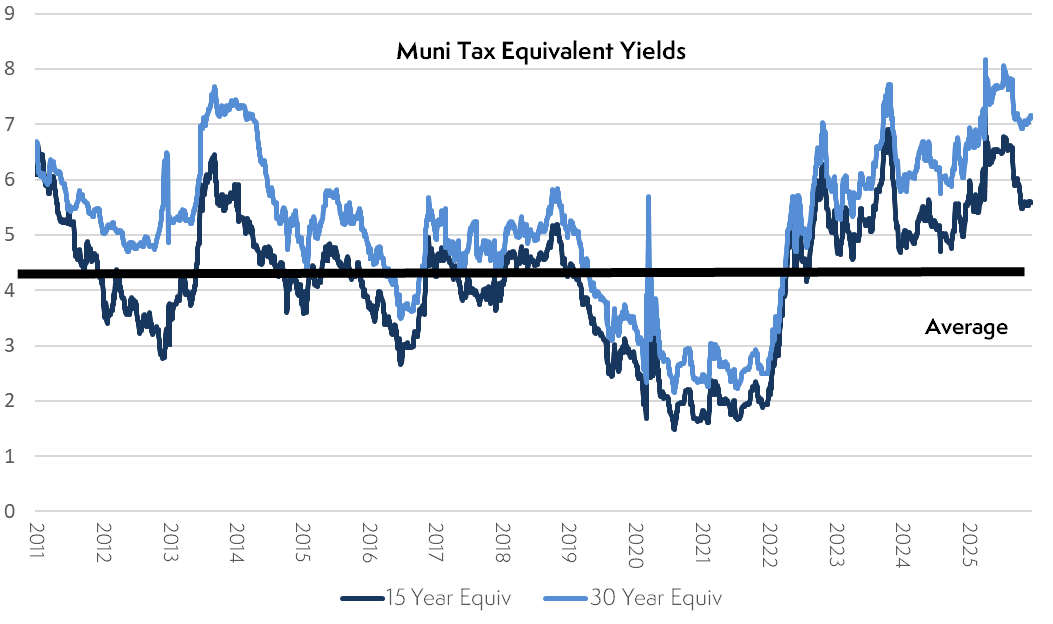

- Attractive relative value. While tax-equivalent yields are down from their summer 2025 peaks, they remain attractive relative to the past 15 years. Municipals continue to offer value.

2026 Muni Market Outlook:

After a difficult first eight months of 2025, municipals attempted to recover but ultimately lagged other fixed income sectors. Municipals returned approximately 4.25 percent, compared with 6.34 percent for U.S. Treasuries and 7.64 percent for U.S. corporates, based on Bloomberg composite indices.

As we enter 2026, MainLine sees several positive fundamental and technical indicators suggesting municipals will avoid another disappointing year.

- Increased demand. As money market yields fall, cash that has been sitting in money funds, much of it for more than a decade, is likely to move into longer-term fixed income.

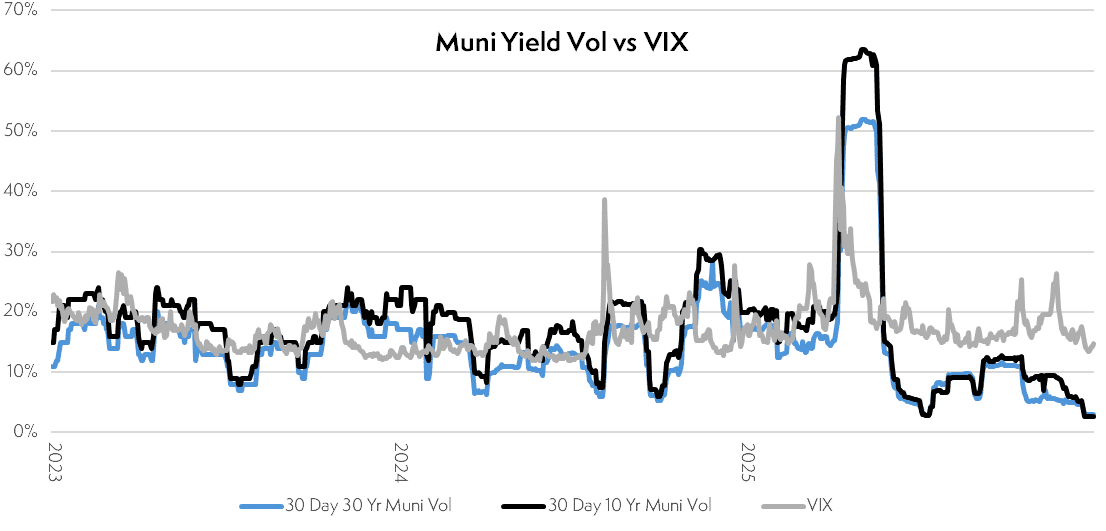

- Greater market certainty. After a turbulent 2025, the market has gained clarity on political risks and the Fed’s direction. The Muni Fear Index declined significantly in the second half of 2025 and remains low. Historically, municipals perform better in periods of low and stable volatility.

- Historical rebound patterns. Municipals have a strong track record of rebounding after underperforming years. Over the past 25 years, municipals have outperformed in six of the eight years following an underperformance year. The two exceptions occurred during periods of elevated volatility.

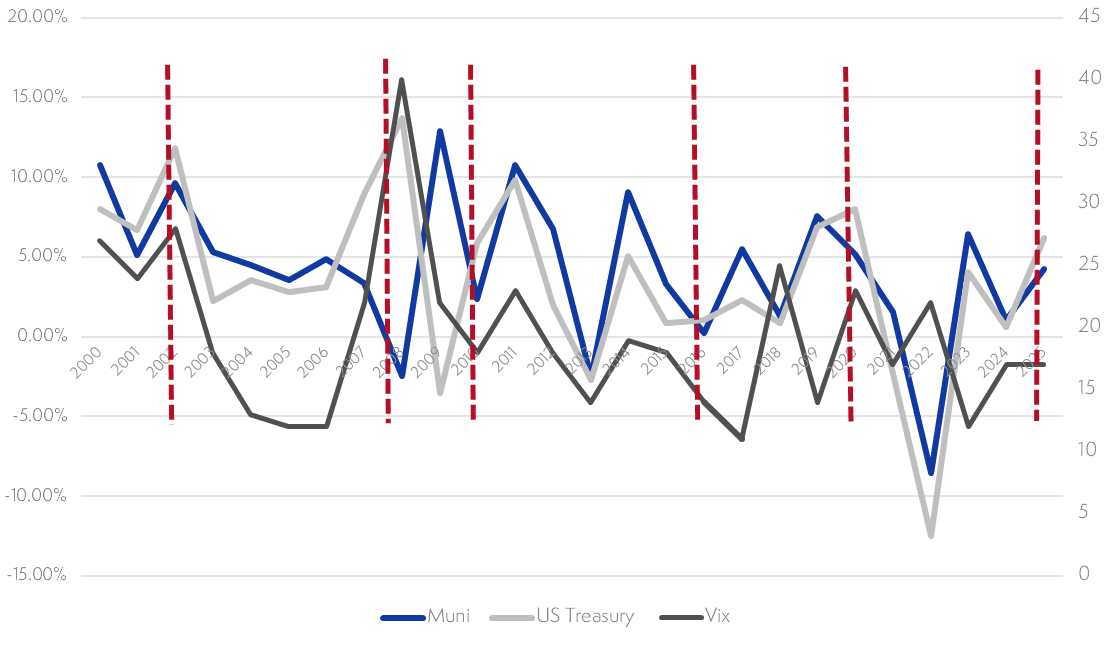

- More market certainty following a turbulent 2025. The market has begun to understand both the political “red storm” and the Federal Reserve’s path forward. This shift is reflected in the Muni Fear Index, which moved significantly lower and remained subdued throughout the second half of 2025. Municipal yield volatility and the VIX are important indicators of municipal performance. Historically, municipals tend to underperform during periods of elevated and erratic volatility, while they outperform during periods of low and stable market movement. This environment should help rebuild confidence among individual investors and encourage them to lock in longer-term fixed income. The chart below shows that the decline in the 2025 Fear Index is setting the stage for a stronger municipal market in 2026.

- Muni value realized as they have a history of bouncing back after a down year. Periods of municipal bond underperformance are often followed by outperformance, particularly when market volatility is declining. In the last 25 years, Munis have outperformed six out of eight times following an underperforming year. The two times they did not were periods when volatility (Fear Index) remained elevated. The graph on the next page shows the total returns of Munis, US Treasuries, and the VIX index. At each dotted red line, the dark blue line (Munis) is coming off an underperforming year, recovers, and the black line (VIX) is decreasing.

The Continued Commoditization of the Muni Market

The Definition of a commodity is to make interchangeable a product to a process that is available for wide use.

Historically, the municipal market has been a boutique, regionally focused industry designed primarily for individual investors and tailored to the needs of municipalities. While this foundation remains, the past decade has brought meaningful change. The municipal market is increasingly commoditized: still regional in nature, but nationally distributed and scaled for efficiency. This shift has helped absorb growing supply.

The key forces driving commoditization include:

- Growth in ETFs and SMAs

- Increased indexing

- Advances in technology

Growth in ETFs & SMAs:

It is now easier and less expensive for investors to access municipals through SMAs and ETFs that offer instant liquidity and benchmark-driven performance. Five to six dominant firms now account for more than half of all municipal fund flows:

- Black Rock (iShares): Dominant in ETFs, largest inflows & AUM

- Vanguard: Major ETF and strong SMA

- JP Morgan Asset Management: notable ETF, and big mutual fund presence

- Franklin Templeton: Large fund manager

- Nuveen/Invesco: Mid-tier but significant

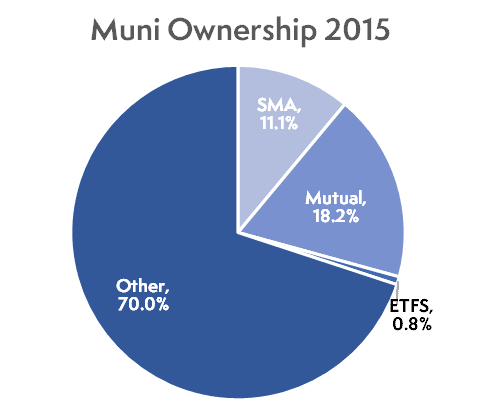

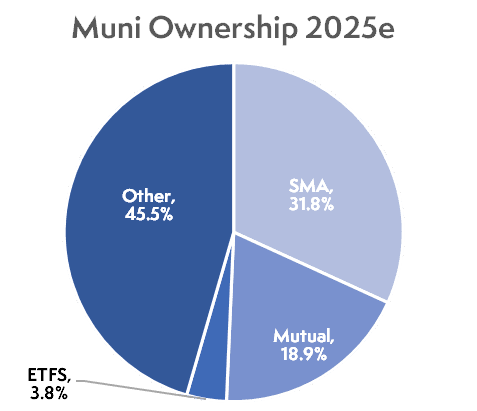

How has this growth in ETFs and SMAs evolved over the years? The charts below show the progression of the Muni market from individual managed to “professionally managed” over the last decade. In the chart, “other” refers to banks, insurance firms and individuals. SMA, ETFs and, mutual funds make up the “professional” group. The pie charts show how the buyer base is changing, and so must the business of selling Munis. SMAs, ETFs and mutual funds now make up over half of the Muni ownership vs 30% ten

years ago. How has this increase in professional management commoditized Munis? It is about making things easier for the “big boys” as they request the following:

- Large bond terms that can be defined as index eligible

- Large deal sizes that allow efficient capital deployment

- Easy to analyze credit quality by having someone else do it. Yes, it’s all about credit ratings and bond insurance

- The ability to create other Muni market products to cross-sell, such as the capacity to short ETFs, “customized” ETFs, and partnering with private entities.

Indexing the Muniverse:

MainLine conducted an extensive review on indexing in its May 2025 Monthly Review: “Dissecting the Indexing Muni Market”. To justify their “professional” management skills, an index is needed to measure the performance of the Funds and SMAs. What better way to perform at the index then to dictate bonds to be “index eligible” and then buy them. It is a self-fulfilling prophecy. How do they do this? Large Muni deals are being termed up for the big buyer to make it “index-eligible”. For example, instead of issuing multiple maturities between 2046 and 2049, issuers may create a single 2050 maturity, with sinking fund payments from 2046 to 2049, producing a larger, index-eligible bond.

Technology:

Technology has made municipal investing more accessible than ever. Platforms such as Schwab and E*Trade allow investors to purchase municipal products from major firms with ease. Data, analytics, and increasingly artificial intelligence guide decision-making.

Electronic distribution has increased, while reliance on individual salespeople has declined. Large deals can now be priced and distributed efficiently, though this efficiency comes at a cost: reduced customization and potentially lower income for less informed investors. Municipals are increasingly delivered to the masses rather than tailored individually.

MainLine understands these changes are needed to price and distribute the growing Muni market. It may be sending shivers up the spine of the “old-timer” as it is creating a more bifurcated market of big versus little issuers and big versus little buyers. While this evolution may unsettle traditional participants, it also creates an opportunity to add value for individual investors.

Bifurcation of the Muni Market:

The rise of indexing, consolidation among major managers, algorithmic trading, and electronic distribution is creating a more bifurcated municipal market. Large issuers benefit from increased liquidity and access to large buyers, while smaller issuers face higher costs and reduced liquidity. Similarly, large buyers gain efficiency, while smaller buyers must navigate a more standardized marketplace. This bifurcation presents both challenges and opportunities, particularly for investors who understand where value still exists outside the most commoditized segments of the market.

How does Commoditization impact MainLine West and its clients?

MainLine sees value in the commoditization and further bifurcation of the Muni market. It creates an opportunity for our clients to add tax-efficient income from issuers and sectors ignored by the Big Five. MainLine focuses on principal-safe, small-issue, non-index municipal bonds that typically offer higher income, greater customization, and broader diversification. Today, more than half of “professional” municipal managers are effectively buying the same bonds for very different investors, commoditizing not only the market, but the investor base itself. We will explore this topic more in 2026 in a monthly review.

Munis and the Affordable Housing Crisis:

The NYC mayoral race has highlighted the affordable housing problem in the USA. How does this impact the Muni market? Once again, the Muni industry is at the forefront of social change, just like it was for climate change. There are major cities that have, in recent years, issued bonds backed by tax revenue to build affordable housing for their residents. In 2025, MainLine purchased bonds issued by a resort town designed to provide affordable housing to its local workforce. For example, Big Sky Ski resort in Montana, Telluride, Grand Junction, and Vail, Colorado. MainLine also participated in affordable housing-related deals in New York City and Philadelphia.

In 2026, MainLine expects municipalities to allocate more tax dollars toward affordable housing for lower-income residents. This may include higher taxes or new fees to fund development. Municipal bonds are well-suited to play a meaningful role in addressing the housing crisis by offering lower borrowing costs through tax-exempt financing, financial accountability, and demographic expertise. These initiatives also provide cities with opportunities to revitalize aging and underutilized infrastructure.

While the municipal market alone cannot solve the affordable housing problem, it should be part of the solution. Ultimately, broader federal involvement will be required. MainLine will explore the role municipals can play in greater depth in a monthly review during 2026.

Munis & AI:

The AI (artificial intelligence) boom is making its impact in also increase issuance. A recent Barclays research report reviews the impact AI is having on the electric and water utility sector as it increases the need for power and infrastructure. AI data centers need high amounts of electricity and water to fuel and cool operations. This has created a need for additional sources of power and water adding to more infrastructure needs. This will create additional costs that will impact issuers and be passed on to its residents. There will likely be some negative credit quality implications in the sector. Issuers in older, smaller, with less diverse fuel sources located in lower wealth regions will be the issuers hit the hardest. Those in wealthy regions with multiple and newer sources of power will be less impacted.

MainLine believes the overall credit implications will remain manageable, as utilities are essential services, and political intervention is likely when needed. One outcome is certain: consumers will ultimately pay higher prices to support the infrastructure behind AI-driven growth.

AI is also increasingly used by municipal investment firms for research, analysis, and, in some cases, portfolio management. While AI can efficiently process data and reduce costs, MainLine believes there is a clear line between using AI as a tool and allowing it to make investment decisions. In our experience, AI excels at gathering information, but evaluating relevance, risk, and portfolio fit remains best handled by experienced municipal professionals.

Other 2026 Trends and Thoughts:

Sector Outlooks:

MainLine likes:

- Housing – Extra income, more principal protection

- Airports – The growth in travel, the evolution of the modern facility is quite impressive and profitable.

- Hospitals affiliated with major health care networks. The improvements in efficiencies and cost savings from the economies of scale.

MainLine does not like:

- Electric utilities in small rural areas with limited supply sources – The demand from AI and the ever-changing energy plan will create challenges to meet supply and increase costs.

- Hospitals in small rural areas – They continue to have labor shortage and DC healthcare politics only add to the financial strain.

Higher Education – Small colleges are under financial pressure.

Credit Quality Outlook:

Credit quality in 2026 will be quiet and will not cause a ripple in the Muni pond. While municipal credit remains strong, the pace of improvement is slowing. The ratio of upgrades to downgrades declined from roughly 2-to-1 in 2023 to an estimated 1.25-to-1 in 2025, and 2026 could approach parity.

Tariffs may also weigh on revenues for manufacturing-heavy states such as Michigan, Kentucky, Tennessee, Indiana, and Illinois, as well as major port states including New Jersey, Texas, California, Georgia, and South Carolina.

2026 Election Year:

It will most likely will not change the Muni dynamics in DC in the near term, but how does the red storm do and how does it look for 2028? Does Mamdani’s win signal a changing of the tide? This could become a big factor in 2027, but MainLine does not feel it will be one in 2026. It also seems such a long way off, but worth a thought, as DC politics never go away for Munis.

What Could Go Wrong with 2026 Outlook?

- Fed is wrong and inflation returns. If rate cuts in 2026 fail to materialize and uncertainty returns, municipals could struggle. Munis need a predictable, calm interest rate environment to find serenity.

- The Red storm is not over, and we are currently sitting in its eye and not in a calm pool. Renewed policy uncertainty could place Munis back in the crossfire between more tax cuts, exempt status, and bipartisan bickering affecting state autonomy and federal funding.

- MainLine is wrong about Muni demand growth, or more likely we are too early. Munis struggle with supply, illiquidity, and uncertainty, and investors stay away. Munis do not become bigger and better.

2026 Outlook Conclusions:

- MainLine feels Munis are primed for a quiet, clip the coupon year and will slowly make up for last year’s dismal performance. By year-end, ratios should improve, with some outperformance. However, the size of the new issue market will keep Munis from getting too rich and too far ahead in performance.

- Investors should look to stay invested and redeploy cash in moments of technical weakness during the year. The ups and downs will not be measurable like they were in 2025 and the yield on cash will continue to decrease. MainLine likes the longer end of the Muni curve, with relative value being strong from 15 years out to 25 years,

- Municipal bonds continue to evolve from a locally focused market designed for individual investors into a more standardized, commoditized product distributed to the masses, with an increasing divide between large and small issuers and buyers. As this shift continues, investors must learn how to navigate modern distribution channels to identify the right bonds while preserving income, diversification, and customization.

- There is still a lot more the Muniverse can do for its residents. Let’s hope the people in DC and financial markets can better appreciate the benefits of municipal finance. Few countries possess an infrastructure financing system as effective as the U.S. municipal market, which remains the envy of much of the world. MainLine will explore this more in a monthly review in the upcoming year.

- MainLine recognizes that investors have many options for tax-exempt investing, many of which appear simpler or more standardized. MainLine offers experience, flexibility, and a personalized approach that large firms cannot replicate. We manage municipals for clients, not as commodities.

MainLine West Happenings in 2025:

- MW welcomed Catherine (Cate) Caselli, joining her two brothers as their baby sister. The parents, Anthony and Lauren, are now playing zone defense, and no longer playing man-to-man. Good luck!

- MW lost several long-time clients and friends as they passed away in 2025. We will miss them, and they will always have a place in our memories, helping us become who we are today.

- Successfully executed Fund VIII at peak tax-equivalent yields, positioning it to deliver approximately 9 percent tax-exempt income.

- Developed an AI model that processes between 350 and 1,000 pages of source material per issuer, extracting key information, summarizing complex data, and generating a clear, data-rich 10 to 15-page credit profile and score. These reports help us determine whether an issuer aligns with a portfolio’s investment objectives, risk parameters, and thematic goals.

Go Team MainLine West!

MainLine Tax Advantaged Opportunity funds have become a top ten TOB floater issuer. TOB floaters are the financing vehicle that the MainLine West Tax Advantaged Opportunity Funds sell to money market funds to leverage their returns. This is a common type of financing for closed-end funds and, as of November 2025, MainLine West represented 4.4% of the $25 billion market. This places MainLine alongside some of the largest closed-end fund managers in the industry, like Nuveen, Invesco, BlackRock and a few other notables.

Entering its 18th year, MainLine will introduce a new product, the Dynamic Fund, designed for active management with managed liquidity and no term-length. Like the Opportunity Funds, the fund will maintain the high credit quality and tax-free income our clients expect. Additional details will be shared in the first quarter of 2026.

We would like to thank all of you for your continued commitment to MainLine West, even through some crazy Muni times. The best is yet to come for Munis and for MainLine West.